India's Household Debt Boom: A Subprime Crisis in the Making?

India's economic growth narrative has long been underpinned by robust domestic consumption. However, recent trends indicate a shift towards increased reliance on debt to fuel this consumption, raising concerns about financial stability. The surge in unsecured personal loans, primarily for consumption rather than asset creation, mirrors patterns observed in the U.S. subprime mortgage crisis. This blog delves into the data and trends that suggest India could be on the brink of a similar financial upheaval.

|

| Data Contrary:- Economic Survey Of India |

The Surge in Household Debt

As of June 2024, India's household debt stood at 42.9% of GDP, a significant rise from 36.6% in June 2021 . This increase is primarily driven by a surge in unsecured personal loans, which grew by 20.6% year-on-year in the first half of FY25 . Notably, unsecured loans now constitute 19.7% of GDP, reflecting a growing reliance on short-term credit for consumption.

Consumption Over Asset Creation

A concerning trend is the shift in borrowing patterns towards consumption rather than asset creation. Data indicates that nearly 50% of loans taken by subprime borrowers are for consumption purposes, compared to 64% of loans by super-prime borrowers used for asset creation . This shift suggests that lower-income groups are increasingly using debt to finance daily expenses, making them more vulnerable to economic shocks.

Declining Household Savings

Parallel to the rise in debt is a decline in household savings. Net financial savings dropped to a 47-year low of 5.3% of GDP in FY23, down from an average of 7.6% between 2011-12 and 2019-20 . This decline indicates that households are not only borrowing more but also saving less, exacerbating financial vulnerabilities.

Rising Non-Performing Assets (NPAs)

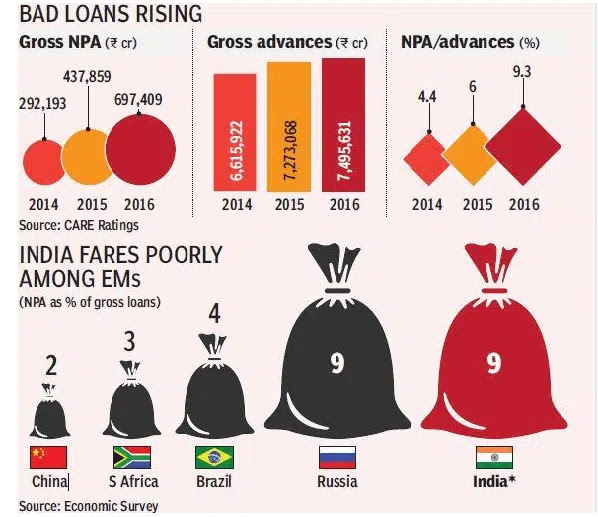

The increase in unsecured lending has led to a rise in NPAs. Credit card NPAs grew by 136% from ₹2,404 crore in March 2020 to ₹5,679 crore by June 2024 . Similarly, personal loan NPAs increased by 51% over the same period. These trends suggest that borrowers are struggling to meet repayment obligations, raising concerns about the health of the financial system.

|

| Data Contrary:- IMF |

Regulatory Response

The Reserve Bank of India (RBI) has issued multiple warnings:

In November 2023, RBI increased risk weights on unsecured consumer loans by 25%, making it costlier for banks to lend.

RBI Governor Shaktikanta Das warned that “unchecked growth in unsecured credit can lead to systemic stress.”

The RBI’s Financial Stability Report (Dec 2023) noted rising delinquency rates in personal loans among borrowers aged 25–35.

The Subprime Parallel: What Happened in the U.S.

The U.S. subprime mortgage crisis was characterized by excessive lending to borrowers with poor credit histories, leading to widespread defaults and a global financial crisis. India's current trajectory, with rising unsecured lending to subprime borrowers for consumption, mirrors these patterns. Without corrective measures, India risks facing a similar crisis. The 2008 Subprime Crisis in the U.S. was sparked by the mass issuance of loans to borrowers with poor credit histories (subprime), mostly for home purchases. When interest rates rose and asset prices fell, defaults soared. This led to:

•Massive bank collapses (Lehman Brothers)

•Global recession

•Loss of trillions in market capitalization

The core issue: loans issued based on credit optimism rather than repayment capacity, backed by the assumption that "prices and demand will keep going up."

Conclusion

India's growing reliance on debt-driven consumption, declining savings, and rising NPAs in the unsecured segment present a precarious situation. While the RBI's regulatory measures are steps in the right direction, a comprehensive approach involving financial literacy, prudent lending practices, and robust risk assessment is essential to avert a potential crisis. Policymakers, financial institutions, and consumers must collaborate to ensure sustainable economic growth without compromising financial stability.

Comments

Post a Comment